Business , Finance

Business & Finance in the Modern World: Strategies, Trends, and Sustainable Growth

Introduction: The Changing Face of Business and Finance

Over the past two decades, the world of business and finance has undergone a dramatic transformation. What once depended heavily on physical infrastructure, manual record-keeping, and localized markets has now evolved into a highly connected, digital-first ecosystem. Today, businesses are no longer limited by geographical boundaries, and financial decisions are increasingly driven by data, analytics, and real-time insights.

In this modern era, success in business is not defined solely by capital or scale. Instead, it depends on adaptability, strategic planning, financial intelligence, and the ability to leverage emerging technologies. Whether you are an entrepreneur, investor, or corporate leader, understanding the dynamics of business and finance is essential for long-term growth and stability.

This article explores the core principles, emerging trends, and practical strategies shaping the future of business and finance.

The Foundation of Business: Strategy and Value Creation

At its core, every successful business is built on a clear strategy and a strong value proposition. Strategy defines the direction of a company—what it aims to achieve and how it plans to get there. Without a well-defined strategy, even well-funded businesses can struggle to survive.

Value creation, on the other hand, is about solving real problems for customers. Companies that focus on delivering meaningful value are more likely to build trust, retain customers, and sustain growth over time.

Modern businesses must answer three critical questions:

What problem are we solving?

Who are we solving it for?

Why should customers choose us over competitors?

These questions form the backbone of any successful business model.

Financial Management: The Backbone of Stability

While strategy drives growth, financial management ensures sustainability. Poor financial planning is one of the leading causes of business failure, even among companies with strong products or services.

Effective financial management includes:

Budgeting: Planning income and expenses to avoid overspending.

Cash Flow Management: Ensuring there is enough liquidity to meet daily operations.

Profitability Analysis: Understanding where profits come from and where losses occur.

Investment Planning: Allocating resources wisely to maximize returns.

A business may generate high revenue, but if it fails to manage its cash flow, it can still collapse. This is why financial discipline is just as important as innovation.

The Rise of Digital Transformation

Digital transformation has become a defining feature of modern business. From small startups to multinational corporations, companies are adopting digital tools to streamline operations, improve customer experiences, and enhance decision-making.

Technologies such as cloud computing, artificial intelligence, and automation are reshaping industries. Businesses can now:

. Analyze large volumes of data in seconds

. Automate repetitive tasks

. Offer personalized customer experiences

. Operate remotely with global teams

For example, e-commerce platforms have revolutionized retail, while fintech solutions have simplified financial transactions and banking services.

Companies that fail to embrace digital transformation risk becoming obsolete in an increasingly competitive market.

Entrepreneurship: Opportunities and Challenges

Entrepreneurship has become more accessible than ever. With the internet providing global reach, individuals can start businesses with relatively low investment. However, ease of entry also means increased competition.

Successful entrepreneurs share several key traits:

. Strong problem-solving skills

. Willingness to take calculated risks

. Adaptability in changing environments

. Persistence in the face of failure

Despite the opportunities, entrepreneurship comes with challenges such as market uncertainty, financial risk, and operational complexity. Many startups fail within the first few years due to poor planning, lack of funding, or inability to scale.

To succeed, entrepreneurs must combine creativity with discipline and continuously refine their strategies based on market feedback.

Investment Strategies: Building Wealth Over Time

Investment is a critical component of financial growth, both for individuals and businesses. Instead of relying solely on active income, investments allow money to grow over time through compounding.

Common investment options include:

. Stocks and equities

. Real estate

. Mutual funds and ETFs

. Bonds and fixed-income securities

Each investment type carries its own level of risk and return. A well-balanced portfolio typically includes a mix of assets to reduce risk while maximizing potential gains.

Long-term investing is generally more effective than short-term speculation. Patience, research, and consistency are key factors in successful investing.

Risk Management: Preparing for Uncertainty

Every business and financial decision involves some level of risk. The goal is not to eliminate risk entirely but to manage it effectively.

Risk management involves:

. Identifying potential threats

. Assessing their impact

. Developing strategies to minimize damage

Common risks include market fluctuations, economic downturns, regulatory changes, and operational disruptions.

Businesses often use tools such as insurance, diversification, and contingency planning to reduce risk exposure. In finance, diversification is particularly important—it ensures that losses in one area do not significantly impact overall performance.

The Role of Innovation in Business Growth

Innovation is the driving force behind long-term success. Companies that continuously innovate are better equipped to adapt to changing market conditions and customer preferences.

Innovation can take many forms:

. Product innovation (new or improved products)

. Process innovation (more efficient operations)

. Business model innovation (new ways of delivering value)

For example, subscription-based models have transformed industries like software and entertainment. Similarly, digital payment systems have changed how transactions are conducted globally.

Organizations that encourage creativity and experimentation are more likely to stay ahead of competitors.

Globalization: Expanding Beyond Borders

Globalization has opened up new opportunities for businesses to expand into international markets. Companies can now reach customers worldwide, source materials from different regions, and build diverse teams.

However, globalization also introduces challenges such as:

. Cultural differences

. Regulatory compliance

. Currency fluctuations

. Supply chain complexities

To succeed globally, businesses must adapt their strategies to local markets while maintaining a consistent brand identity.

Personal Finance: The Foundation of Financial Security

While business finance focuses on organizations, personal finance is equally important for individuals. Managing personal finances effectively can lead to financial independence and long-term security.

Key aspects of personal finance include:

. Saving and budgeting

. Managing debt

. Investing wisely

. Planning for retirement

Financial literacy plays a crucial role in making informed decisions. Individuals who understand basic financial principles are better equipped to avoid debt traps and build wealth over time.

The Impact of Technology on Finance (FinTech)

Financial technology, or fintech, has revolutionized the way people manage money. From mobile banking apps to digital wallets, fintech solutions have made financial services more accessible and efficient.

Key innovations in fintech include:

. Online payment systems

. Peer-to-peer lending platforms

. Cryptocurrency and blockchain technology

. Robo-advisors for investment management

These technologies have reduced the need for traditional intermediaries, making transactions faster and more cost-effective.

However, they also raise concerns about data security and regulatory oversight, which must be addressed to ensure long-term trust.

Sustainable Business Practices

Sustainability has become a major focus in modern business. Companies are increasingly expected to operate responsibly, considering environmental, social, and governance (ESG) factors.

Sustainable practices include:

. Reducing carbon emissions

. Using renewable resources

. Ensuring fair labor practices

. Supporting community development

Businesses that prioritize sustainability not only contribute to a better world but also attract customers and investors who value ethical practices.

Leadership and Decision-Making

Strong leadership is essential for navigating the complexities of business and finance. Leaders are responsible for setting the vision, making strategic decisions, and guiding teams toward success.

Effective leaders possess:

. Clear communication skills

. Emotional intelligence

. Strategic thinking abilities

. Accountability and integrity

Decision-making in business often involves uncertainty. Leaders must analyze data, consider risks, and make informed choices quickly.

A good leader does not rely solely on intuition but balances it with evidence and experience.

Future Trends in Business and Finance

The future of business and finance will be shaped by several key trends:

1. Artificial Intelligence: Increasing automation and smarter decision-making

2. Remote Work: Flexible work environments becoming the norm

3. Digital Currencies: Growing interest in decentralized finance

4. Data-Driven Strategies: Greater reliance on analytics and insights

5. Sustainability Focus: Stronger emphasis on ethical and environmental responsibility

Businesses that anticipate and adapt to these trends will be better positioned for long-term success.

Conclusion: Building a Strong Financial Future

Business and finance are deeply interconnected fields that play a crucial role in shaping economies and individual lives. Success in these areas requires a combination of strategic thinking, financial discipline, innovation, and adaptability.

In a rapidly changing world, those who stay informed, embrace technology, and make data-driven decisions will have a significant advantage. Whether you are running a business, investing in markets, or managing personal finances, the principles remain the same: plan wisely, act responsibly, and continuously seek improvement.

The journey toward financial growth and business success is not a one-time effort but an ongoing process. With the right mindset and strategies, sustainable growth is not only possible—it is achievable.

Running an online store is about much more than picking trending products or running clever ad campaigns. The businesses that actually last are the ones that master something far less glamorous: cash flow. A store can look profitable on paper and still collapse if money isn’t moving through it the right way.

Cash flow simply means the money coming into your business versus the money going out. Sales bring cash in. Inventory, ads, software subscriptions, shipping, and taxes take cash out. When inflow outpaces outflow, you’re in good shape. When it’s the other way around, even a store with strong sales numbers can end up scrambling to pay its bills.

Ecommerce makes this trickier than most businesses. You often have to spend money before you ever see a sale — stocking inventory, running ad campaigns, building out your website, paying for fulfillment. If those upfront costs aren’t managed with a clear plan, a store that looks successful from the outside can quietly be running on fumes.

This guide breaks down what cash flow actually looks like for an online store, why it matters so much, where most stores run into trouble, and what you can do about it.

What Cash Flow Really Means for an Online Store

Profit and cash flow are not the same thing, and confusing the two is one of the most common mistakes new store owners make. Profit is what’s left after you subtract costs from revenue, on paper. Cash flow is whether you actually have money sitting in your account when you need it.

Picture a store that brings in $25,000 in sales during a month. That sounds healthy. But if a chunk of that revenue is tied up with a payment processor for several days, and supplier invoices are due now, that store could be cash-poor even while looking profitable in its sales reports. This happens more often than people expect, and it’s usually the businesses growing the fastest that feel it the most, simply because their expenses are scaling right alongside their sales.

A lot of moving pieces affect ecommerce cash flow on any given day. Revenue from product sales is the obvious one, but the cost of purchasing or restocking inventory, shipping and fulfillment, ad spend, recurring software fees, payment processing fees, and money lost to returns and refunds all pull in the opposite direction. Because these hit your accounts at different times, timing ends up mattering just as much as the totals themselves. A business that only checks “are we profitable” without also asking “do we have cash on hand right now” is flying half-blind.

Why Cash Flow Keeps the Lights On

People call cash flow the lifeblood of a business for good reason. Without it, nothing else really functions, no matter how good your products or marketing are.

Every store has bills that don’t wait. Ad budgets need topping up, platform subscriptions renew automatically, customer service tools need paying for, and processing fees get deducted from every sale whether you’re ready for them or not. If cash isn’t available when these come due, operations start to stall, sometimes in ways that are hard to reverse quickly.

Inventory is one of the biggest cash traps in ecommerce. Buying stock ties up capital long before that stock turns into revenue, and store owners who over-invest in inventory often find themselves short on cash for the marketing or growth moves that would actually move the needle. This is part of why dropshipping and supplier-fulfillment models have become so popular over the past few years. Sourcing through platforms that let you sell without buying bulk inventory upfront frees up capital that would otherwise sit on a warehouse shelf collecting dust.

Growth costs money too. A new product line, a bigger ad budget, a website redesign — all of it requires cash before it pays off. Stores with healthy cash flow can jump on these opportunities the moment they appear. Stores without it tend to watch competitors move first, and by the time they catch up, the window has often closed.

Where Ecommerce Stores Typically Run Into Trouble

The pace of online retail creates cash flow problems that look a little different from a traditional brick-and-mortar business.

Sales rarely stay flat throughout the year. Black Friday and the holiday season can bring a flood of revenue, while January and February often go quiet by comparison. Stores that don’t plan for that swing can find themselves short on cash exactly when the slower months hit, even right after a record-breaking quarter. It’s a strange position to be in — celebrating your best month ever and worrying about cash flow at the same time — but it happens constantly in this industry.

Paid traffic is often non-negotiable for ecommerce growth, and ad costs have a way of climbing faster than anyone expects. Platforms like Google, Meta, and TikTok reward constant reinvestment, and it’s easy for spend to outpace what’s actually coming back in, especially during the testing phase of a new campaign when results are still unpredictable.

Stocking physical inventory means paying upfront for products that might take weeks or months to sell through. Money sitting in unsold stock isn’t money you can use anywhere else, which is exactly why so many sellers have been shifting toward leaner, supplier-fulfilled inventory models instead of buying in bulk and hoping it sells.

And then there’s the simple delay built into how payments work. Most processors don’t release funds the instant a sale happens. There’s often a few days’ lag before money actually lands in your account, and that gap can create a short-term crunch right when a supplier payment or ad invoice happens to be due.

How to Actually Track Your Cash Flow

You can’t manage what you don’t measure, and tracking cash flow properly means looking at both sides of the ledger consistently, not just glancing at your bank balance every now and then.

Start with the basics — knowing exactly where your income comes from (product sales, subscriptions, affiliate revenue) and where it’s going (inventory, marketing, software, fulfillment). This sounds obvious, but a surprising number of store owners couldn’t tell you, off the top of their head, what their three biggest monthly expenses actually are.

A cash flow statement helps formalize this. It usually breaks into three parts: operating activity, which covers day-to-day sales and costs; investing activity, covering equipment or technology purchases; and financing activity, covering loans or outside funding. Reviewing this regularly, even informally, helps catch problems while they’re still small.

Forecasting matters just as much as looking backward. Projecting expected revenue, upcoming marketing spend, and supplier payments for the months ahead lets you prepare for slow periods instead of being caught off guard by them. It doesn’t need to be perfect — even a rough estimate beats no plan at all.

Practical Ways to Improve Your Cash Flow

Improving cash flow mostly comes down to making sure money comes in faster than it goes out, without choking off the spending that actually drives growth.

Rethinking how you stock inventory is usually the biggest lever available. Instead of sinking cash into large inventory orders, a leaner model — supplier-fulfillment or dropshipping — lets you offer a wide product catalog without locking up capital in unsold stock. That keeps more cash available for the parts of the business that actually generate growth.

Suppliers are often more flexible than store owners assume, but only if you ask. Extended payment terms, bulk discounts, or structured payment plans are all things worth negotiating for. Getting better terms can mean you sell the product and collect revenue before the supplier payment is even due, which flips the usual cash flow problem on its head.

Margins matter more than most people give them credit for. Every extra point of margin is extra cash from the exact same sales volume, and bundling products, introducing premium variants, or trimming unnecessary costs all stretch margins further without needing a single additional sale.

Ad spend deserves regular scrutiny rather than a set-it-and-forget-it mindset. Killing underperforming campaigns quickly and redirecting that budget toward what’s actually converting sounds simple, but a lot of stores let weak campaigns run far longer than they should, quietly draining cash over a quarter.

Software subscriptions are another quiet leak. Most stores accumulate tools over time, some genuinely useful and others forgotten but still billing every month. A periodic audit of what you’re actually paying for tends to turn up easy savings almost every time.

Shipping costs eat into margin fast if left unchecked, and partnering with reliable, fast suppliers — including ones offering fulfillment from US and EU warehouses — can cut both cost and delivery time at once. Faster, cheaper shipping ends up helping cash flow and customer satisfaction simultaneously.

Automation helps too. Automated email flows, order processing, and chatbot-driven support let a store scale without scaling costs at the same rate. The less manual labor something requires, the more breathing room there is to grow without bleeding cash in the process.

Build a Cash Reserve Before You Need One

One of the simplest ways to protect a store from a cash crunch is to keep a financial buffer on hand before there’s ever a problem. A reserve gives you breathing room when sales dip unexpectedly, an ad account underperforms for no clear reason, or a supplier shipment gets delayed at the worst possible time.

Most financial advisors suggest keeping somewhere between three and six months of operating expenses in reserve. It’s not glamorous advice, and it’s easy to put off building one, but it’s often the difference between riding out a rough quarter calmly and scrambling for emergency funding under pressure.

Metrics Worth Watching Closely

A handful of numbers tell you most of what you need to know about a store’s cash health. Gross profit margin shows how much revenue remains after product costs, and higher margins simply mean more cash left over per sale. Customer acquisition cost shows what it costs to land each new customer, and lowering it frees up cash for other priorities. Inventory turnover rate shows how quickly stock sells and gets replaced, with faster turnover meaning less capital sitting idle on a shelf somewhere. Operating cash flow shows how much cash a business generates purely from its core activity, and a reliably positive number is usually the clearest sign of real financial stability.

A Few Mistakes That Quietly Drain Cash

Even store owners who pay close attention to their numbers fall into a few recurring traps that slowly eat away at available cash without ever showing up as one obvious red flag.

It’s tempting to reinvest revenue the moment it lands, but a portion of every sale is already earmarked for processing fees, returns, and taxes. Spending against gross revenue instead of actual net cash on hand is one of the fastest ways to end up short without realizing why.

Scaling ad spend before a campaign has proven itself is another common one. Pouring more budget into something that hasn’t shown a consistent, profitable return burns through reserves quickly, and it’s usually worth letting a campaign prove itself on a smaller budget first.

Small recurring charges add up in ways that are easy to miss. A $15 app subscription doesn’t feel like much on its own, but stack a dozen of them across marketing, analytics, and automation tools, and they start to resemble a meaningful monthly drain that often goes unnoticed until someone finally does a full audit.

Return rates get underestimated too, particularly in categories like apparel where they tend to run high. They can quietly shrink net cash flow even when gross sales numbers look strong, so building expected return rates into your forecasting upfront avoids an unpleasant surprise later on.

When It Makes Sense to Bring in Outside Financing

Sometimes good habits aren’t quite enough to cover a short-term gap, and that’s not necessarily a sign something’s wrong. Seasonal businesses in particular often need a bridge between a slow month and the next big sales push.

Short-term financing — a line of credit, supplier credit terms, or revenue-based funding — can smooth over these gaps without forcing a store to pause marketing or restock inventory at the wrong moment. The key is treating financing as a planned tool rather than a last-minute rescue. A store that lines up access to capital before it’s desperately needed ends up in a far stronger position than one scrambling during an actual crisis.

Final Thoughts

Cash flow really is what keeps an ecommerce business alive day to day. Sales numbers and profit margins matter, but if there isn’t cash available when bills come due, none of that matters very much.

Tracking money in and out consistently, forecasting ahead, tightening up inventory and ad spend, and keeping a reserve for rough patches gives store owners the financial footing to grow without constantly worrying about what’s actually in the bank.

None of this requires complicated finance software or an accounting degree. It mostly requires consistency — reviewing numbers regularly, adjusting early when something looks off, and treating cash flow as a core part of running the business rather than an afterthought. That discipline tends to be exactly what separates the stores that survive a few tough months from the ones that don’t.

Meta Description

Learn how a small business line of credit works, its benefits, requirements, costs, and smart funding strategies to improve cash flow and grow your business successfully.

Introduction

Every business owner faces financial challenges at some point. Sometimes sales are strong, but customer payments arrive late. Other times, inventory must be purchased before revenue comes in. Unexpected expenses, marketing opportunities, equipment repairs, and seasonal demand can all create situations where immediate access to capital becomes essential.

This is why many entrepreneurs turn to a small business line of credit. Unlike traditional business loans that provide a fixed lump sum, a business line of credit offers flexible access to funds whenever they are needed. It acts as a financial safety net while helping businesses manage cash flow, seize growth opportunities, and maintain daily operations.

Whether you run an eCommerce store, consulting agency, healthcare practice, SaaS company, retail business, or local service company, understanding how a line of credit for small business works can help you make smarter financial decisions.

In this comprehensive guide, you’ll learn everything about business lines of credit, including benefits, qualification requirements, interest rates, funding strategies, common mistakes, and how to determine if this financing option is right for your business.

What Is a Small Business Line of Credit?

A small business line of credit is a flexible financing solution that gives businesses access to a predetermined credit limit. Rather than borrowing a large amount at once, business owners can withdraw only the amount they need and repay it over time.

As repayments are made, the available credit becomes accessible again. This revolving structure allows businesses to continuously borrow and repay funds without submitting a new application every time financing is needed.

Think of it as a business version of a credit card but often with higher limits and more favorable borrowing terms.

For example:

. Approved credit limit: $50,000

. Amount borrowed: $10,000

. Interest charged only on: $10,000

The remaining $40,000 remains available for future use.

This flexibility makes a business line of credit one of the most popular forms of working capital financing.

Why Small Businesses Need Flexible Financing

Running a business is rarely predictable.

Expenses often occur before revenue arrives.

Common situations include:

. Purchasing inventory before peak sales seasons

. Covering payroll during slow payment cycles

. Launching marketing campaigns

. Paying suppliers

. Managing unexpected repairs

. Expanding operations

. Hiring additional employees

Without access to capital, these situations can limit growth.

A business funding solution like a revolving credit line helps companies remain financially stable while continuing to grow.

How a Business Line of Credit Works

The process is straightforward.

Step 1: Apply for Funding

The lender evaluates:

. Business revenue

. Time in operation

. Credit history

. Financial statements

. Cash flow performance

Based on this information, a credit limit is approved.

Step 2: Access Funds

Once approved, businesses can withdraw funds whenever necessary.

Many lenders provide:

. Online account access

. Mobile banking options

. Direct transfers to business accounts

Step 3: Make Payments

Businesses repay borrowed amounts according to agreed terms.

Monthly payments may include:

. Principal repayment

. Interest charges

. Applicable fees

Step 4: Reuse Available Credit

As funds are repaid, available credit increases again.

This revolving feature is what separates a business line of credit from a traditional loan.

Types of Small Business Lines of Credit

Understanding the different options helps businesses choose the best financing solution.

Secured Business Line of Credit

A secured credit line requires collateral.

Examples include:

. Real estate

. Equipment

. Inventory

. Accounts receivable

. Business savings

Benefits

. Lower interest rates

. Higher credit limits

. Better approval odds

Drawbacks

. Risk of losing collateral

. Longer approval process

Unsecured Business Line of Credit

An unsecured credit line does not require collateral.

Approval depends mainly on:

. Business performance

. Revenue history

. Personal credit score

. Financial stability

Benefits

. Faster approvals

. No collateral required

. Lower business risk

Drawbacks

. Higher interest rates

. Smaller funding limits

Benefits of a Small Business Line of Credit

1. Better Cash Flow Management

Cash flow problems are one of the leading reasons businesses struggle.

Revenue and expenses rarely align perfectly.

A business cash flow management strategy supported by a line of credit allows companies to:

. Cover short-term expenses

. Maintain operations

. Avoid late payments

This helps create financial stability.

2. Flexible Access to Working Capital

Unlike loans that provide a lump sum, a line of credit gives businesses flexibility.

Borrow only what you need when you need it.

This reduces unnecessary debt and borrowing costs.

3. Interest Charged Only on Used Funds

One of the biggest advantages is cost efficiency.

Interest applies only to the borrowed amount.

For example:

If approved for $100,000 but only use $15,000, interest applies only to $15,000.

This makes a small business line of credit a highly efficient funding option.

4. Emergency Financial Protection

Unexpected events happen frequently.

Examples include:

. Equipment breakdowns

. Supplier delays

. Emergency repairs

. Legal expenses

. Technology failures

A credit line acts as a financial safety net.

5. Support Business Growth

Growth often requires upfront investment.

Businesses can use credit lines for:

. Inventory expansion

. Hiring staff

. Product launches

. Advertising campaigns

. New office locations

This makes a business growth funding strategy easier to execute.

6. Improve Business Credit

Responsible borrowing and repayment can strengthen your business credit profile.

Benefits include:

. Better financing options

. Lower interest rates

. Higher future funding limits

. Improved lender confidence

Common Uses for a Business Line of Credit

Inventory Purchases

Many retailers and eCommerce stores need inventory before sales occur.

A credit line helps businesses:

. Purchase stock

. Prepare for seasonal demand

. Prevent stock shortages

Marketing Campaigns

Marketing requires upfront spending.

Businesses frequently use credit lines for:

. Google Ads

. Facebook Ads

. SEO campaigns

. Email marketing

. Influencer partnerships

A strong return on investment can make these expenses highly profitable.

Payroll Management

Employee salaries must be paid on time.

A line of credit helps businesses cover payroll during temporary revenue gaps.

Equipment Repairs

Unexpected breakdowns can interrupt operations.

A revolving credit line provides immediate funding for repairs and replacements.

Seasonal Business Operations

Seasonal businesses often experience uneven revenue.

Examples include:

. Tourism

. Retail

. Landscaping

. Holiday-related businesses

A line of credit helps bridge off-season periods.

Potential Drawbacks

Although useful, business lines of credit are not perfect.

Variable Interest Rates

Many lenders use variable rates.

This means borrowing costs can increase over time.

Always review lender terms carefully.

Additional Fees

Possible fees include:

. Annual fees

. Maintenance fees

. Draw fees

. Renewal fees

. Late payment fees

Compare lenders carefully.

Risk of Overspending

Easy access to capital can encourage excessive borrowing.

Business owners should avoid using credit lines as a substitute for profitability.

Qualification Challenges

Some lenders have strict requirements.

New businesses may face:

. Higher rates

. Lower limits

. Additional guarantees

How to Qualify for a Small Business Line of Credit

Most lenders evaluate several factors.

Revenue

Consistent revenue demonstrates repayment ability.

Higher revenue often leads to:

. Better rates

. Larger limits

. Faster approvals

Credit Score

Both personal and business credit scores matter.

Strong credit can improve funding opportunities.

Time in Business

Many lenders prefer businesses operating for:

. 6 months minimum

. 12+ months preferred

. 2+ years for premium terms

Financial Records

Lenders review:

. Profit and loss statements

. Tax returns

. Bank statements

. Cash flow reports

Accurate financial records improve approval chances.

Documents Required

Prepare the following:

Financial Documents

. Business bank statements

. Tax returns

. Profit and loss statements

. Balance sheets

Business Documents

. Business registration

. Operating agreements

. Ownership information

. EIN documentation

Personal Information

. Identification

. Credit history

. Contact details

Having documentation ready speeds up the application process.

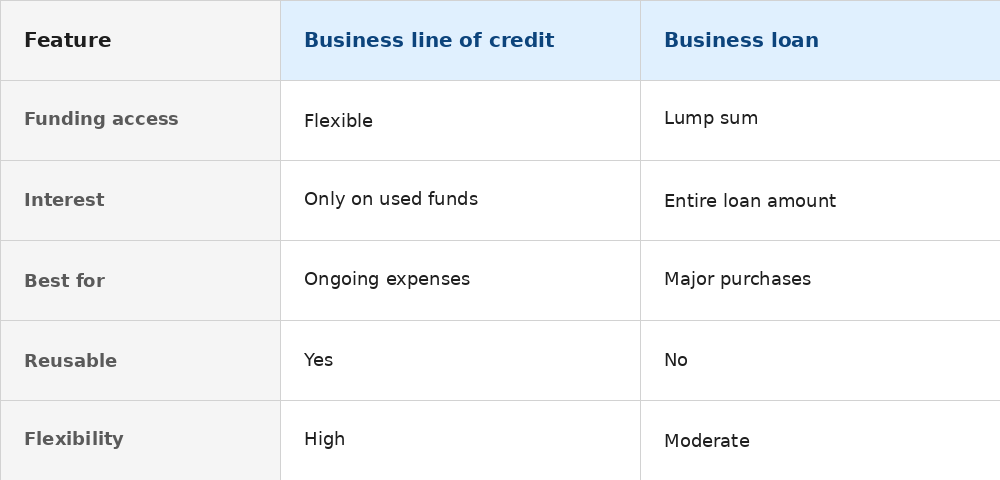

Business Line of Credit vs Business Loan

Choose a Credit Line If:

. Cash flow fluctuates

. Expenses vary monthly

. Working capital is needed regularly

Choose a Loan If:

. Purchasing equipment

. Buying property

. Funding major expansion

Smart Strategies for Using a Business Credit Line

Use It for Revenue-Generating Activities

The best borrowing creates future income.

Examples include:

. Marketing campaigns

. Product inventory

. Sales expansion

. Customer acquisition

Avoid Maxing Out Your Limit

Maintaining low utilization improves financial flexibility.

Many experts recommend staying below 30-50% utilization whenever possible.

Repay Early

Early repayment reduces:

. Interest costs

. Debt burden

. Financial risk

It also restores available credit faster.

Track Spending Carefully

Use accounting software to monitor:

. Borrowed amounts

. Repayments

. Interest costs

. Cash flow impact

Mistakes to Avoid

Using Credit for Personal Expenses

Keep business and personal finances separate.

Ignoring Fee Structures

Some lenders advertise low rates but charge significant fees.

Missing Payments

Late payments damage business credit.

Borrowing Without a Plan

Always understand:

. Why funds are needed

. Expected return

. Repayment strategy

Is a Small Business Line of Credit Right for You?

A business line of credit is ideal if:

✅ You have consistent revenue.

✅ You need working capital flexibility.

✅ You experience seasonal cash flow gaps.

✅ You want emergency funding access.

✅ You plan to grow your business.

It may not be ideal if:

❌ Your business is consistently losing money.

❌ You cannot manage repayments.

❌ You need long-term fixed financing.

Frequently Asked Questions

What credit score is needed for a business line of credit?

Most lenders prefer scores above 600, while premium lenders often look for 680+.

Can startups qualify?

Yes, although funding limits may be smaller and rates may be higher.

Does a business line of credit build credit?

Yes. Responsible use and on-time payments can improve your business credit profile.

Are business credit lines better than loans?

It depends on your needs. Credit lines offer flexibility, while loans are better for large one-time purchases.

Can an LLC get a business line of credit?

Yes. Most lenders offer funding solutions specifically for LLCs and incorporated businesses.

Conclusion

A small business line of credit remains one of the most valuable financing tools available today. It provides flexible access to capital, helps businesses manage cash flow, supports growth opportunities, and creates a financial safety net during uncertain periods.

Whether you’re managing inventory, covering payroll, launching marketing campaigns, or handling unexpected expenses, a well-managed business credit line can strengthen your company’s financial position and support long-term success.

By understanding the costs, benefits, qualification requirements, and best practices discussed in this guide, business owners can make informed financing decisions and build a stronger foundation for sustainable growth.

Introduction

The startup landscape continues to evolve as technology advances, consumer behavior changes, and new opportunities emerge across industries. In 2026, aspiring entrepreneurs have more opportunities than ever to build profitable businesses with relatively low startup costs. Digital tools, artificial intelligence, remote work solutions, and global connectivity have significantly reduced barriers to entry.

However, starting a successful business is not simply about following trends. The most successful startups solve real problems, provide genuine value, and adapt quickly to changing market demands. Whether you’re a student, freelancer, corporate employee, or experienced entrepreneur, choosing the right startup idea can be the first step toward long-term success.

This guide explores some of the most promising startup ideas for 2026 and explains why they have strong growth potential in today’s business environment.

Why 2026 Is a Great Time to Start a Business

Several factors make 2026 an attractive year for entrepreneurs.

First, digital technology has become more accessible. Businesses can launch websites, automate operations, manage customer relationships, and market products without significant upfront investments.

Second, consumers are increasingly comfortable purchasing products and services online. From education and healthcare to consulting and retail, digital business models continue to grow rapidly.

Third, artificial intelligence is helping startups operate more efficiently. Small teams can now accomplish tasks that previously required large departments, allowing entrepreneurs to compete more effectively.

Finally, remote work has expanded access to global talent and international customers, creating opportunities that were difficult to achieve just a few years ago.

1. AI Consulting Services

Artificial intelligence is transforming nearly every industry. Many businesses understand the importance of AI but struggle to implement it effectively.

An AI consulting startup can help organizations identify automation opportunities, integrate AI tools, improve workflows, and train employees.

As AI adoption continues to grow, businesses will increasingly seek expert guidance to maximize efficiency and maintain competitiveness.

2. Content Marketing Agency

Businesses consistently need high-quality content to attract customers, improve search rankings, and establish authority.

A content marketing agency can offer services such as:

. Blog writing

. SEO content creation

. Copywriting

. Content strategy

. Email marketing campaigns

As competition online increases, demand for professional content continues to expand.

3. SaaS Development

Software-as-a-Service remains one of the most profitable startup models available.

Instead of selling one-time products, SaaS companies generate recurring revenue through subscriptions.

Potential SaaS niches include:

. Project management

. Customer relationship management

. HR software

. Marketing automation

Successful SaaS businesses often benefit from predictable income and strong scalability.

4. Ecommerce Brand

Ecommerce continues to grow worldwide.

Entrepreneurs can launch niche online stores focusing on specific customer needs rather than competing directly with large marketplaces.

Examples include:

. Eco-friendly products

. Home office equipment

. Fitness accessories

. Pet products

. Personalized gifts

A focused niche often allows businesses to build stronger customer loyalty and brand recognition.

5. Digital Marketing Services

Every business needs visibility online.

A digital marketing startup can provide:

. Search engine optimization

. Social media management

. Pay-per-click advertising

. Email marketing

. Analytics reporting

As businesses continue investing in online growth, marketing services remain in high demand.

6. Online Education Platforms

The e-learning industry has experienced tremendous growth over the past decade.

Entrepreneurs can create online courses covering topics such as:

. Technology

. Business skills

. Design

. Personal development

. Language learning

With proper expertise and quality content, educational businesses can generate recurring revenue for years.

7. Virtual Assistant Agency

Many business owners need administrative support but do not require full-time employees.

A virtual assistant agency can provide services such as:

. Email management

. Appointment scheduling

. Customer support

. Data entry

. Research assistance

This startup model requires relatively low investment and can scale efficiently.

8. Cybersecurity Services

Cyber threats continue to increase as businesses become more dependent on digital infrastructure.

Organizations require assistance with:

. Security audits

. Risk assessments

. Employee training

. Data protection

. Compliance management

Cybersecurity startups have strong long-term growth potential due to increasing digital risks.

9. Personal Finance Coaching

Many individuals struggle with budgeting, saving, investing, and debt management.

A personal finance coaching business can help clients improve financial literacy and make better money decisions.

Growing awareness of financial wellness creates opportunities for experts who can provide practical guidance.

10. Health and Wellness Business

Health-conscious consumers continue to seek products and services that improve their well-being.

Potential opportunities include:

. Online fitness coaching

. Nutrition consulting

. Wellness memberships

. Mental health support resources

The wellness industry remains one of the fastest-growing sectors globally.

11. Remote Work Solutions

Remote and hybrid work environments have become standard for many organizations.

Businesses need tools and services that support distributed teams.

Potential startup ideas include:

. Team collaboration platforms

. Productivity software

. Remote employee training

. Virtual team-building services

Demand for remote work solutions is expected to remain strong.

12. Web Design and Development

Every modern business requires an effective online presence.

A web design startup can help companies create:

. Professional websites

. Ecommerce stores

. Landing pages

. Mobile-friendly experiences

Businesses continually update their digital presence, creating ongoing opportunities for web professionals.

13. Influencer Marketing Agency

Brands increasingly collaborate with creators to reach targeted audiences.

An influencer marketing startup can manage:

. Campaign planning

. Influencer outreach

. Performance tracking

. Partnership negotiations

As social media continues to dominate digital attention, influencer marketing remains a valuable business opportunity.

14. Subscription Box Business

Subscription models provide predictable recurring revenue.

Examples include:

. Beauty products

. Fitness supplements

. Pet supplies

. Books

. Specialty foods

Customers appreciate convenience and curated experiences, making subscription businesses attractive.

15. Mobile App Development

Mobile applications continue to shape consumer behavior.

Businesses and entrepreneurs often need custom applications for:

. Customer engagement

. Productivity

. Ecommerce

. Education

. Entertainment

Developers who create valuable solutions can build highly scalable businesses.

Key Factors for Startup Success

While choosing the right idea is important, execution matters even more.

Successful startups typically focus on:

Solving Real Problems

Businesses that address genuine customer challenges are more likely to gain traction.

Understanding the Market

Research helps entrepreneurs identify customer needs, competitors, and opportunities.

Building Strong Branding

A memorable brand increases trust and encourages customer loyalty.

Prioritizing Customer Experience

Satisfied customers often become repeat buyers and recommend businesses to others.

Adapting Quickly

Markets change rapidly. Startups that remain flexible can respond more effectively to new opportunities and challenges.

Common Startup Mistakes to Avoid

Many startups fail due to avoidable mistakes.

Common issues include:

. Lack of market research

. Poor financial management

. Ignoring customer feedback

. Overcomplicating products

. Weak marketing strategies

Entrepreneurs who learn from these mistakes can significantly improve their chances of success.

Conclusion

The opportunities available to entrepreneurs in 2026 are broader than ever before. Advances in technology, growing digital adoption, and changing consumer expectations continue to create new markets and business models.

Whether you choose to launch an AI consulting firm, ecommerce brand, SaaS platform, marketing agency, or educational business, success ultimately depends on delivering value and solving meaningful problems.

The best startup idea is not necessarily the newest trend. It is the idea that aligns with your skills, interests, and ability to serve customers effectively. By focusing on execution, customer satisfaction, and continuous improvement, entrepreneurs can build sustainable businesses that thrive in the years ahead.

How to Set a Marketing Budget for Your Dropshipping Store (Without Wasting Money)

Best Ecommerce Analytics Tools for Dropshippers in 2026

Customer Experience Automation: What It Is and Why It Matters

The Transformative Benefits of Artificial Intelligence in Modern Life

AI, SaaS, SEO & Link Building: The New Operating System of Digital Growth

Why Email Marketing Still Drives Real Business Growth in 2026

-

Tech , SaaS2 months ago

Tech , SaaS2 months agoThe Transformative Benefits of Artificial Intelligence in Modern Life

-

Tech , SaaS2 months ago

Tech , SaaS2 months agoAI, SaaS, SEO & Link Building: The New Operating System of Digital Growth

-

Email Marketing2 months ago

Email Marketing2 months agoWhy Email Marketing Still Drives Real Business Growth in 2026

-

Sports , Fashion2 months ago

Sports , Fashion2 months agoSports & Fashion: The Perfect Blend of Performance, Style, and Modern Lifestyle

-

Email Marketing2 months ago

Email Marketing2 months agoEmail Marketing in 2026: The Ultimate Strategy for Growth, Engagement, and Conversions

-

Health , Education2 months ago

Health , Education2 months agoHealth and Education: The Foundation of a Strong and Successful Society

-

Business , Finance2 months ago

Business , Finance2 months agoThe New Economy: How Digital Innovation, Behavioral Finance, and Smart Systems Are Redefining Global Business

-

Email Marketing2 months ago

Email Marketing2 months agoThe Future of Customer Communication: Smart Email Systems, Automation, and Digital Engagement in 2026