Business , Finance

Small Business Line of Credit Benefits and Funding Guide

Meta Description

Learn how a small business line of credit works, its benefits, requirements, costs, and smart funding strategies to improve cash flow and grow your business successfully.

Introduction

Every business owner faces financial challenges at some point. Sometimes sales are strong, but customer payments arrive late. Other times, inventory must be purchased before revenue comes in. Unexpected expenses, marketing opportunities, equipment repairs, and seasonal demand can all create situations where immediate access to capital becomes essential.

This is why many entrepreneurs turn to a small business line of credit. Unlike traditional business loans that provide a fixed lump sum, a business line of credit offers flexible access to funds whenever they are needed. It acts as a financial safety net while helping businesses manage cash flow, seize growth opportunities, and maintain daily operations.

Whether you run an eCommerce store, consulting agency, healthcare practice, SaaS company, retail business, or local service company, understanding how a line of credit for small business works can help you make smarter financial decisions.

In this comprehensive guide, you’ll learn everything about business lines of credit, including benefits, qualification requirements, interest rates, funding strategies, common mistakes, and how to determine if this financing option is right for your business.

What Is a Small Business Line of Credit?

A small business line of credit is a flexible financing solution that gives businesses access to a predetermined credit limit. Rather than borrowing a large amount at once, business owners can withdraw only the amount they need and repay it over time.

As repayments are made, the available credit becomes accessible again. This revolving structure allows businesses to continuously borrow and repay funds without submitting a new application every time financing is needed.

Think of it as a business version of a credit card but often with higher limits and more favorable borrowing terms.

For example:

. Approved credit limit: $50,000

. Amount borrowed: $10,000

. Interest charged only on: $10,000

The remaining $40,000 remains available for future use.

This flexibility makes a business line of credit one of the most popular forms of working capital financing.

Why Small Businesses Need Flexible Financing

Running a business is rarely predictable.

Expenses often occur before revenue arrives.

Common situations include:

. Purchasing inventory before peak sales seasons

. Covering payroll during slow payment cycles

. Launching marketing campaigns

. Paying suppliers

. Managing unexpected repairs

. Expanding operations

. Hiring additional employees

Without access to capital, these situations can limit growth.

A business funding solution like a revolving credit line helps companies remain financially stable while continuing to grow.

How a Business Line of Credit Works

The process is straightforward.

Step 1: Apply for Funding

The lender evaluates:

. Business revenue

. Credit history

. Financial statements

. Cash flow performance

Based on this information, a credit limit is approved.

Step 2: Access Funds

Once approved, businesses can withdraw funds whenever necessary.

Many lenders provide:

. Online account access

. Mobile banking options

. Direct transfers to business accounts

Step 3: Make Payments

Businesses repay borrowed amounts according to agreed terms.

Monthly payments may include:

. Principal repayment

. Interest charges

. Applicable fees

Step 4: Reuse Available Credit

As funds are repaid, available credit increases again.

This revolving feature is what separates a business line of credit from a traditional loan.

Types of Small Business Lines of Credit

Understanding the different options helps businesses choose the best financing solution.

Secured Business Line of Credit

A secured credit line requires collateral.

Examples include:

. Real estate

. Equipment

. Inventory

. Accounts receivable

. Business savings

Benefits

. Lower interest rates

. Higher credit limits

. Better approval odds

Drawbacks

. Risk of losing collateral

. Longer approval process

Unsecured Business Line of Credit

An unsecured credit line does not require collateral.

Approval depends mainly on:

. Business performance

. Revenue history

. Personal credit score

. Financial stability

Benefits

. Faster approvals

. No collateral required

. Lower business risk

Drawbacks

. Higher interest rates

. Smaller funding limits

Benefits of a Small Business Line of Credit

1. Better Cash Flow Management

Cash flow problems are one of the leading reasons businesses struggle.

Revenue and expenses rarely align perfectly.

A business cash flow management strategy supported by a line of credit allows companies to:

. Cover short-term expenses

. Maintain operations

. Avoid late payments

This helps create financial stability.

2. Flexible Access to Working Capital

Unlike loans that provide a lump sum, a line of credit gives businesses flexibility.

Borrow only what you need when you need it.

This reduces unnecessary debt and borrowing costs.

3. Interest Charged Only on Used Funds

One of the biggest advantages is cost efficiency.

Interest applies only to the borrowed amount.

For example:

If approved for $100,000 but only use $15,000, interest applies only to $15,000.

This makes a small business line of credit a highly efficient funding option.

4. Emergency Financial Protection

Unexpected events happen frequently.

Examples include:

. Equipment breakdowns

. Supplier delays

. Emergency repairs

. Legal expenses

. Technology failures

A credit line acts as a financial safety net.

5. Support Business Growth

Growth often requires upfront investment.

Businesses can use credit lines for:

. Inventory expansion

. Hiring staff

. Product launches

. Advertising campaigns

. New office locations

This makes a business growth funding strategy easier to execute.

6. Improve Business Credit

Responsible borrowing and repayment can strengthen your business credit profile.

Benefits include:

. Better financing options

. Lower interest rates

. Higher future funding limits

. Improved lender confidence

Common Uses for a Business Line of Credit

Inventory Purchases

Many retailers and eCommerce stores need inventory before sales occur.

A credit line helps businesses:

. Purchase stock

. Prepare for seasonal demand

. Prevent stock shortages

Marketing Campaigns

Marketing requires upfront spending.

Businesses frequently use credit lines for:

. Google Ads

. Facebook Ads

. SEO campaigns

. Email marketing

. Influencer partnerships

A strong return on investment can make these expenses highly profitable.

Payroll Management

Employee salaries must be paid on time.

A line of credit helps businesses cover payroll during temporary revenue gaps.

Equipment Repairs

Unexpected breakdowns can interrupt operations.

A revolving credit line provides immediate funding for repairs and replacements.

Seasonal Business Operations

Seasonal businesses often experience uneven revenue.

Examples include:

. Tourism

. Retail

. Landscaping

. Holiday-related businesses

A line of credit helps bridge off-season periods.

Potential Drawbacks

Although useful, business lines of credit are not perfect.

Variable Interest Rates

Many lenders use variable rates.

This means borrowing costs can increase over time.

Always review lender terms carefully.

Additional Fees

Possible fees include:

. Annual fees

. Maintenance fees

. Draw fees

. Renewal fees

. Late payment fees

Compare lenders carefully.

Risk of Overspending

Easy access to capital can encourage excessive borrowing.

Business owners should avoid using credit lines as a substitute for profitability.

Qualification Challenges

Some lenders have strict requirements.

New businesses may face:

. Higher rates

. Lower limits

. Additional guarantees

How to Qualify for a Small Business Line of Credit

Most lenders evaluate several factors.

Revenue

Consistent revenue demonstrates repayment ability.

Higher revenue often leads to:

. Better rates

. Larger limits

. Faster approvals

Credit Score

Both personal and business credit scores matter.

Strong credit can improve funding opportunities.

Time in Business

Many lenders prefer businesses operating for:

. 6 months minimum

. 12+ months preferred

. 2+ years for premium terms

Financial Records

Lenders review:

. Profit and loss statements

. Tax returns

. Bank statements

. Cash flow reports

Accurate financial records improve approval chances.

Documents Required

Prepare the following:

Financial Documents

. Business bank statements

. Tax returns

. Profit and loss statements

. Balance sheets

Business Documents

. Business registration

. Operating agreements

. Ownership information

. EIN documentation

Personal Information

. Identification

. Credit history

. Contact details

Having documentation ready speeds up the application process.

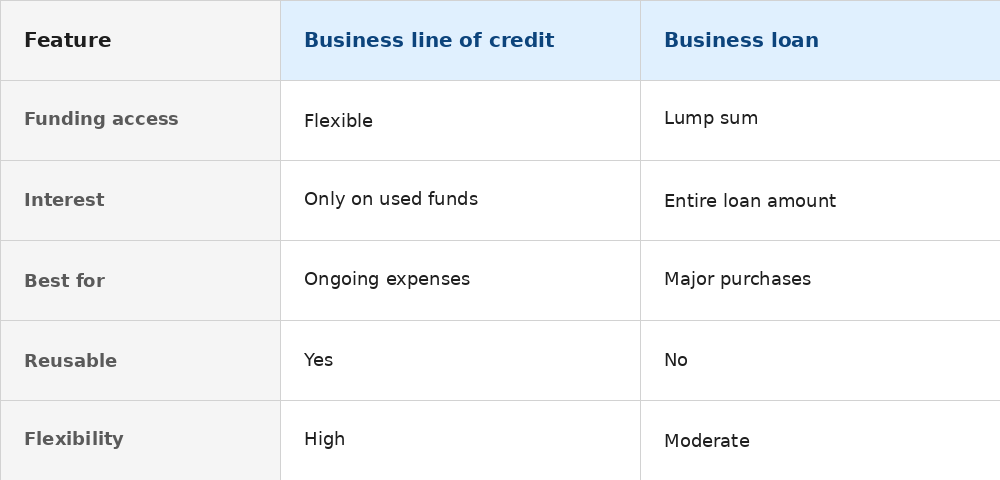

Business Line of Credit vs Business Loan

Choose a Credit Line If:

. Cash flow fluctuates

. Expenses vary monthly

. Working capital is needed regularly

Choose a Loan If:

. Purchasing equipment

. Buying property

. Funding major expansion

Smart Strategies for Using a Business Credit Line

Use It for Revenue-Generating Activities

The best borrowing creates future income.

Examples include:

. Marketing campaigns

. Product inventory

. Sales expansion

. Customer acquisition

Avoid Maxing Out Your Limit

Maintaining low utilization improves financial flexibility.

Many experts recommend staying below 30-50% utilization whenever possible.

Repay Early

Early repayment reduces:

. Interest costs

. Debt burden

. Financial risk

It also restores available credit faster.

Track Spending Carefully

Use accounting software to monitor:

. Borrowed amounts

. Repayments

. Interest costs

. Cash flow impact

Mistakes to Avoid

Using Credit for Personal Expenses

Keep business and personal finances separate.

Ignoring Fee Structures

Some lenders advertise low rates but charge significant fees.

Missing Payments

Late payments damage business credit.

Borrowing Without a Plan

Always understand:

. Why funds are needed

. Expected return

. Repayment strategy

Is a Small Business Line of Credit Right for You?

A business line of credit is ideal if:

✅ You have consistent revenue.

✅ You need working capital flexibility.

✅ You experience seasonal cash flow gaps.

✅ You want emergency funding access.

✅ You plan to grow your business.

It may not be ideal if:

❌ Your business is consistently losing money.

❌ You cannot manage repayments.

❌ You need long-term fixed financing.

Frequently Asked Questions

What credit score is needed for a business line of credit?

Most lenders prefer scores above 600, while premium lenders often look for 680+.

Can startups qualify?

Yes, although funding limits may be smaller and rates may be higher.

Does a business line of credit build credit?

Yes. Responsible use and on-time payments can improve your business credit profile.

Are business credit lines better than loans?

It depends on your needs. Credit lines offer flexibility, while loans are better for large one-time purchases.

Can an LLC get a business line of credit?

Yes. Most lenders offer funding solutions specifically for LLCs and incorporated businesses.

Conclusion

A small business line of credit remains one of the most valuable financing tools available today. It provides flexible access to capital, helps businesses manage cash flow, supports growth opportunities, and creates a financial safety net during uncertain periods.

Whether you’re managing inventory, covering payroll, launching marketing campaigns, or handling unexpected expenses, a well-managed business credit line can strengthen your company’s financial position and support long-term success.

By understanding the costs, benefits, qualification requirements, and best practices discussed in this guide, business owners can make informed financing decisions and build a stronger foundation for sustainable growth.

Leaving agency work or a public sector role to start your own therapy practice is one of the most significant career moves a therapist can make. The clinical freedom is real, but so is the sudden responsibility of running a business alongside your caseload. This checklist walks through everything worth having in place, from legal groundwork through to the daily systems that keep a practice running smoothly, so you can launch with confidence rather than guesswork.

Getting Your Legal and Financial Foundation Right

Before you see your first client, a handful of legal and financial steps need to be locked in. Skipping any of these creates risk that tends to surface at the worst possible moment, so treat this section as non negotiable groundwork rather than something to circle back to later.

Choose the Right Business Structure

Most therapists starting out register as a sole trader, which is the simplest structure and suits the majority of new private practitioners. Registering with HMRC for Self Assessment becomes a legal requirement once your earnings pass the trading allowance, and doing this promptly avoids unnecessary penalties. Some therapists eventually move to a limited company as earnings grow, since it can offer tax advantages, though the administrative overhead increases as well. It is worth researching both paths properly before committing.

Register for Data Protection Compliance

Therapists handle some of the most sensitive personal data that exists, which means registration with the Information Commissioner’s Office and payment of the annual data protection fee is almost always required. Compliance here is not optional. You need a clear privacy notice, a documented lawful basis for processing client information, and genuinely secure systems for storing records. Building these habits in from day one, rather than retrofitting them later, saves significant stress down the line.

Separate Your Business and Personal Finances

Opening a dedicated business bank account from the outset keeps your finances clean and your tax returns far simpler. It also makes it much easier to track income and expenses accurately, and it presents a more credible, professional image to clients and accountants alike.

Secure Professional Indemnity Insurance

Professional indemnity insurance is essential before you see a single client. It protects you if someone brings a claim of negligence or harm arising from your work. Most accrediting bodies require current indemnity cover as a condition of membership, so check exactly what level of cover your professional body expects and have the policy active before your doors open.

Arrange Clinical Supervision

Clinical supervision is both an ethical requirement and a practical safeguard, and it needs to be in place before you take on clients, continuing throughout your practice rather than tapering off once you feel established. Look for a supervisor who understands the business and ethical realities of private practice, not just the clinical side, and build supervision costs into your financial planning from the very beginning.

Building a Business Plan That Actually Guides You

Many therapists are drawn to private practice for the clinical independence it offers, but running a sustainable practice still means running a business. Your plan does not need to read like a corporate document. It just needs to give you real clarity on where you are headed and how you intend to get there without running out of money along the way.

Estimate Your Realistic Startup Costs

Launching a therapy practice is considerably cheaper than most other small businesses, but there are still upfront and ongoing costs worth planning for carefully. A typical breakdown might look something like this: directory listings on major platforms tend to run between fifteen and thirty pounds a month for a premium profile, professional indemnity and public liability insurance usually costs one hundred to one hundred fifty pounds annually, room rental by the hour often falls between ten and twenty five pounds, or two hundred to six hundred pounds monthly for a fixed space depending on location, and practice management software subscriptions typically range from twenty to fifty pounds a month.

Having a clear picture of these overhead numbers lets you calculate exactly how many sessions you need to book each month simply to break even, which is a far more useful number than a vague sense of “enough clients.”

What Belongs in Your Plan

A useful plan for a private therapy practice should cover your vision and niche, meaning who you actually want to work with and which therapeutic approaches you will offer. It should include your financial targets, specifically how many client hours per week you need to cover costs and hit your income goals. Your marketing approach deserves its own section too, covering exactly how you intend to attract and retain clients. Overhead costs, including room rental, supervision, continuing professional development, insurance, memberships, software, and your website, should all be itemized rather than estimated loosely. Finally, think through basic risk mitigation: what happens if a client cancels last minute, or your caseload unexpectedly drops for a few weeks.

Setting Fees That Actually Work

Pricing your sessions is one of the more emotionally loaded parts of starting out. Fees set too low leave you financially stretched and prone to burnout. Fees set too high without the experience or reputation to support them can make it harder to fill your caseload in the early months.

Start by calculating your genuine cost per session, factoring in a proportional share of room rental, supervision, continuing education, insurance, and software. From there, look at the going rate for your specialism and area. Many therapists use a sliding scale to keep their services accessible to lower income clients while still maintaining a sustainable overall income, and being transparent about your fee structure from the very first point of contact avoids awkward conversations later.

Getting Your Paperwork and Policies in Order

Before welcoming your first client, your administrative documentation needs to be genuinely ready, not just drafted. This protects you both legally and ethically while setting clear boundaries for the therapeutic relationship from day one.

Every client should complete a secure, compliant intake form covering personal details, relevant history, and emergency contacts before their first session. Equally important is documenting informed consent properly: clients need to explicitly agree to the terms of treatment, understand the limits of confidentiality, and acknowledge your cancellation policy in writing. That cancellation policy should clearly state how much notice is required to avoid a charge, commonly forty eight hours, along with any associated no show fees. Having all of this spelled out in a client contract prevents misunderstandings later and protects the time you have set aside for clinical work.

Navigating the Shift From Clinician to Business Owner

Moving from a clinical role into practice ownership involves a real psychological adjustment, not just a change in job title. As a therapist, your training centers entirely on client wellbeing. As a business owner, you now also carry responsibility for marketing, finances, and administration, and that dual identity can trigger genuine imposter syndrome. Feeling unqualified to run a business, particularly without a commercial background, is an extremely common and entirely normal part of this transition.

The weight of being solely responsible for your own income can feel heavy too. A quiet week can start to feel like personal failure rather than the normal fluctuation that private practice naturally involves. Recognizing this as a standard part of the entrepreneurial shift, rather than a sign something is wrong, matters more than it might seem. Connecting with peer support groups or finding mentors who understand the business side of therapy specifically can make this transition considerably smoother.

Choosing the Right Space to Practice From

Finding the right physical environment for your work is one of the more consequential early decisions you will make, since the space itself directly shapes the therapeutic relationship.

Working From Home Versus Renting a Room

Working from home is appealing for cost reasons, but it comes with genuine practical and ethical considerations. You need a truly private space with proper sound insulation, ideally a separate entrance, and a firm boundary between your personal and professional life. You will also need to inform your mortgage provider or landlord, check your home insurance covers professional use, and think carefully about whether working from home suits your intended client group.

Renting a therapy room is the most common choice for therapists starting out, since many centers offer rooms by the hour or half day, which keeps fixed costs low while your caseload is still building. When evaluating a potential room, weigh accessibility for clients with mobility needs, genuine soundproofing and privacy, whether a waiting area is available, proximity to public transport, and simply whether the space feels right for therapeutic work.

As your caseload grows, moving toward a fixed weekly room rental, or eventually a dedicated space of your own, often makes sense. Keeping costs proportionate to your actual client volume, especially in the early months, protects your cash flow while you build momentum.

Getting Found by the Right Clients

Even excellent therapists need a steady stream of clients finding them. Marketing does not have to feel uncomfortable or at odds with your professional values. At its core, it is simply about making sure people who need your specific help are able to find you.

Where New Clients Actually Come From

For most new practitioners, the most reliable early source of clients is word of mouth and professional referrals. Letting colleagues, local GP surgeries, employee assistance programme providers, and your wider professional network know you are accepting new clients costs nothing and often converts well.

Beyond word of mouth, a few other channels consistently deliver results. Listing your practice on established therapist directories puts you in front of people actively searching with strong booking intent, and a well written, complete profile tends to generate enquiries relatively quickly. A simple, professional website is also worth the investment even alongside directory listings, since it gives you full control over how you present yourself, lets prospective clients learn about your approach before reaching out, and improves how easily local searches find you. It does not need to be elaborate: a clean site covering your approach, fees, and contact details is genuinely sufficient.

Building relationships with other professionals, including GPs, psychiatrists, occupational health teams, and fellow therapists in your area, tends to generate a steady stream of referrals over time. Attending professional body events, joining peer supervision groups, and staying active in professional communities all help raise your profile in ways that compound gradually rather than instantly.

Running the Operational Side Smoothly

Scheduling and Booking

Relying on phone calls and a manual diary tends to create missed bookings, double bookings, and unnecessary administrative burden as your caseload grows. Automating this process frees up meaningful time for clinical work instead.

Integrating online booking directly into your website lets clients schedule appointments securely at their own convenience, updating your calendar in real time and reducing human error. It also captures clients who prefer booking outside standard office hours, which is a growing share of most caseloads. A well set up booking system can allow clients to book outside clinic hours, choose from your live availability, receive automated confirmations and reminders that reduce no shows, and even collect a deposit upfront to help cover your overheads.

Giving Clients Some Control Through a Portal

Offering clients a reasonable degree of control over their own appointments tends to strengthen the working relationship, provided it is balanced sensibly. A well designed client portal can let clients book new appointments, whether virtual or in person, pay a deposit at the time of booking, request a callback if you were unavailable when they first reached out, request their documents be sent securely, settle remaining balances online, and reschedule or cancel with appropriate notice.

Moving Your Notes Fully Digital

Going paperless is a priority for most therapists once they see how much time and risk it removes from note keeping. Digital systems make it considerably easier to create standardized notes that anyone involved in a client’s care can understand quickly, generate properly formatted documents with minimal manual effort, organize information for later analysis and reporting, and sort by document type to build a clear history of what has actually happened over time.

Handling Billing Without It Feeling Transactional

The relationship you build with clients should never feel primarily transactional, even though payment is obviously part of it. Handling billing, invoicing, and payments digitally helps keep the emphasis on the support you are providing rather than the mechanics of getting paid.

A dedicated system typically lets you build a clear schedule with services attached to upcoming appointments, link billing directly to specific sessions so clients know exactly what they are being charged for, take prepayments during booking to help cover overheads in advance, and send automated reminders about any remaining balance. Syncing your invoicing with your accounting software also saves considerable time at tax season and keeps your accountant working from accurate, up to date numbers.

Offering Video Consultations as Standard

Video consultations have become a permanent and fully expected part of how therapy is delivered. Offering virtual sessions as a primary option can dramatically reduce your startup costs and overhead, since it removes room rental from the equation entirely and lets you run a genuinely flexible practice. Hybrid working, where clients choose between in person and online sessions depending on the week, is now the norm rather than the exception, and building this flexibility into your practice model from the start puts you ahead rather than playing catch up later.

A solid telemedicine setup, properly connected to your broader practice management system, lets you manage every appointment type on a single calendar, start video sessions directly from the same platform you use for scheduling, generate reports on how virtual sessions are affecting your practice over time, and send automated reminders that head off technical issues before they disrupt a session.

Frequently Asked Questions

Do I need a DBS check to work as a private therapist?

Whether a Disclosure and Barring Service check is required depends on the nature of your work. If you plan to see children or vulnerable adults, an enhanced check is mandatory. Even with an exclusively adult, non vulnerable caseload, some professional bodies and room rental providers still require a standard or enhanced check as a condition of practice, so confirm requirements with your professional body and any premises you plan to use.

How do I choose a clinical supervisor for private practice?

Look for someone with direct private practice experience of their own, ideally including its business and administrative realities, not just the clinical side. Your supervisor should work within a compatible modality and have a solid grasp of your ethical framework. Ask about their approach, availability, and how they handle urgent concerns between sessions, since this relationship is one of the most important professional connections you will maintain.

What key ethical and contractual requirements need to be in place before seeing clients?

You should have a signed therapeutic contract covering fees, cancellation policy, confidentiality and its limits, your approach, and how sessions will be conducted. You also need active clinical supervision, current professional indemnity insurance, and a clear, compliant privacy notice provided before or at the point of first contact.

Can I start a therapy practice part time or alongside another job?

Yes, and it is a very common, practical approach. Many therapists begin by seeing a few private clients in the evenings or on weekends while keeping a full time role, which reduces financial risk and allows the caseload to build gradually before making a full transition.

What software do therapists typically use to manage their private practice?

Most therapists rely on dedicated practice management platforms that combine scheduling, client records, billing, and telemedicine in a single system, along with features like online booking, compliant note keeping, automated reminders, and integration with standard accounting software.

Final Thoughts

Starting a therapy private practice in the UK involves considerably more than clinical readiness, but none of the business side needs to feel overwhelming when it is broken into clear, sequential steps. Get your legal and financial foundations solid first, build a business plan that actually reflects reality, set fees that let you sustain the work long term, and put simple systems in place for booking, notes, and billing before you need them under pressure. Practices built this deliberately tend to feel steady far sooner than those assembled reactively after clients have already started arriving.

Running a private practice can be deeply rewarding. You get to help people feel better, often on your own terms, without layers of institutional bureaucracy standing between you and the patient. But rewarding does not mean easy. Rising costs, shifting regulations, and a patient market that has more options than ever mean the business side of your practice needs just as much attention as the clinical side.

Clinical skill keeps patients healthy. Business discipline keeps the practice alive long enough to keep helping them. This guide walks through the practical keys to managing a private practice well, from the systems that prevent chaos to the marketing habits that keep new patients coming through the door.

Build a System Before Chaos Builds Itself

Every business benefits from being run with intention rather than instinct, and a private practice is no exception. The starting point is simple: look honestly at where things stand right now, decide where you actually want the practice to go, and write down how you plan to get there.

Every practice has strengths worth leaning on and weaknesses worth addressing. The earlier you identify both, the sooner you can turn that knowledge into better decisions rather than repeated surprises.

A written business plan is not just paperwork for a bank or investor. It becomes the operating foundation for the entire practice. A useful plan describes your services clearly, includes a realistic financial model covering both startup costs and expected revenue, and sets specific objectives with actual deadlines attached. Revisiting this document at least once a year keeps it aligned with where the practice is actually heading, rather than where it was pointed on day one.

Mapping out your organizational structure, even with a simple chart, helps clarify who owns which responsibilities and where duties might currently overlap or fall through the cracks. Talk to your team about how they see the day to day workflow. Their perspective often reveals friction points a founder sitting outside the daily grind never notices. Once you can see the full picture, look specifically for steps that could be simplified, automated, or removed entirely.

From there, take an honest look at who is handling which business processes and whether they are actually equipped to do so well. If a gap exists, whether in billing, scheduling, or general operations, additional training or a targeted new hire is usually a better long term investment than hoping the gap closes itself.

Treat Data Security as Non Negotiable

As your operational systems take shape, data security cannot be an afterthought. Patient information is sensitive by definition, and protecting it requires real cybersecurity measures alongside strict compliance with applicable data protection regulation.

Your practice management software should be fully compliant, properly encrypted, and backed up regularly to secure servers rather than local devices. Routine security audits, paired with regular staff training on data handling protocols, meaningfully reduce the risk of a breach that could otherwise cost both money and patient trust that took years to build.

Get Your Legal and Financial Foundation Right From Day One

Before you see your first patient, your legal and financial groundwork needs to be solid. Skipping or rushing this stage is one of the most common and expensive mistakes new practice owners make.

In England, regulatory registration is a legal requirement for most private practices providing regulated activities such as treatment of disease or diagnostic procedures. Operating without proper registration is a criminal offense, so confirming your specific obligations early and building the registration timeline directly into your business plan is essential rather than optional.

Medical indemnity insurance is equally non negotiable. Every practitioner needs adequate cover in place before treating a single private patient, and that cover should reflect the actual scope of your work, including any procedures, medico legal activity, or telemedicine consultations you plan to offer.

On the financial side, choosing your trading structure early matters. Sole trader status, a limited company, or a partnership each carry different tax implications, and getting advice from an accountant who specifically understands medical practices is worth the investment many times over.

Getting recognized by major private medical insurance networks takes time and involves a formal application process. Once approved, you will need clear billing procedures and software capable of tracking outstanding insurance payments alongside self pay accounts. Streamlining your billing workflow and conducting regular audits reduces claim denials and protects the steady cash flow your practice depends on. As the broader healthcare landscape shifts, it is also worth considering how value based care models, which tie reimbursement to patient outcomes, might eventually complement your traditional fee for service approach.

Choose Your Location and Operating Model Carefully

Deciding where and how to operate is one of the earliest practical decisions you will face, and it shapes patient accessibility, overhead costs, and referral patterns for years to come.

A few factors deserve real weight in this decision. Proximity to your referral base matters if general practitioners are a major source of new patients, since geographic convenience genuinely affects referral volume. Renting space within an established private hospital or clinic can lower your capital costs while giving patients a setting they already trust. Whatever arrangement you choose, understand exactly what is included in the lease, from reception cover to parking to clinical waste disposal, before signing anything.

If you plan to admit or treat patients within a private hospital setting, practicing privileges are typically required first. Each hospital runs its own credentialing process, generally verifying your professional registration, indemnity cover, references, and recent appraisal. This process can take several months, so applying early avoids unnecessary delays to opening.

Strong referral relationships are worth cultivating deliberately. Responding promptly to referral letters, keeping referring clinicians updated on their patients’ progress, and keeping the referral pathway simple all build the kind of professional trust that sustains a practice well beyond its first few years.

Build and Support a Strong Administrative Team

A capable administrative team is the operational backbone of any well run private practice. Many practitioners underestimate how much clinical and administrative work actually overlaps, and the cost of getting this wrong shows up directly in both patient experience and revenue.

A skilled medical secretary handles far more than answering the phone. Their responsibilities typically span appointment booking and rescheduling, processing referral correspondence, chasing insurance authorizations, and supporting medico legal administration. In many ways, a good medical secretary becomes the face of your practice to patients, which makes hiring someone with real healthcare administration experience worth prioritizing.

A few considerations shape how you build this team. Using existing institutional staff for private work during contracted hours or with institutional resources carries real regulatory risk and should be avoided entirely. Deciding whether to hire directly, use a specialist practice management service, or bring in a virtual assistant changes both your costs and your level of oversight, so weigh these options against your actual patient volume rather than defaulting to whichever feels most familiar. Whoever fills the role needs a clear understanding of their scope, including how to handle patient complaints, insurance queries, and urgent clinical messages.

Regular one to one check ins and clear operating protocols help administrative staff work with confidence, which ultimately reflects well on the entire practice. It is also worth staying alert to signs of burnout among both clinical and administrative staff. A high pressure clinic environment takes a real toll over time, and encouraging full breaks, watching for excessive workloads, and creating a culture where people feel safe asking for help all protect your team’s wellbeing and, by extension, your practice’s stability.

Revisit Your Processes Regularly

Build the habit of periodically reviewing your business processes, staff structure, equipment, and software rather than assuming what worked at launch still fits today. Circumstances change as a practice grows, and clinging to workflows that once served you well but now hold you back is a quiet but real drag on performance.

Rethink Where Your Money Actually Goes

Growing revenue should not always be the top priority, which can sound counterintuitive but often proves true in practice. Take a close look at where your current income is actually going and where efficiency gains are hiding in plain sight. Many vendors offer meaningful discounts for purchases made within a specific window, so the next time you update your practice software or equipment, it is worth asking directly about available deals. The same logic applies to utility providers, where switching suppliers can meaningfully reduce recurring costs.

Scheduling deserves close attention too, particularly for your clinicians. Every hour a doctor spends not seeing patients is an hour of lost revenue, so look honestly at what changes could keep your medical staff engaged with patients for more of their working day. Retaining experienced clinical staff matters just as much as optimizing schedules. Practices that invest in staff loyalty, including simple gestures like acknowledging service anniversaries and recognizing hard work, tend to find that experienced practitioners feel genuinely valued and are far less likely to leave for a competitor.

Take Marketing Seriously, Even in Healthcare

Relying solely on word of mouth is a risky strategy for any practice. Building the kind of reputation that generates consistent referrals organically takes years, and there is no guarantee it will produce a steady enough stream of new patients on its own.

A working marketing plan should balance attracting new patients with retaining existing ones, since retention is almost always more cost effective than acquisition. Your website deserves particular attention, since it is often a prospective patient’s very first impression of your practice. It should clearly communicate your areas of expertise, consultation fees, location, and how to book, while loading quickly and working well on mobile devices. Basic search optimization, including location specific keywords and a properly maintained business listing, helps ensure local patients can actually find you.

Patient engagement matters just as much as acquisition. Giving patients easy access to their records and appointment history through a patient portal, actively collecting feedback through post visit surveys, and acting on what that feedback reveals all strengthen retention over time. Community outreach and educational events can also build reputation and attract new patient groups who might not otherwise encounter your practice.

Mapping the full patient journey, from first online search through booking, consultation, and follow up, reveals exactly where friction exists and where small improvements to communication or booking can meaningfully improve both retention and satisfaction.

A few practical marketing steps worth prioritizing: define your brand clearly, including your name, visual identity, and tone of voice; make sure your website includes obvious calls to action like an online booking button or direct phone number; encourage satisfied patients to leave reviews, since social proof builds trust quickly with prospective patients; and track which channels actually bring in new patients so you can invest your time and budget where it counts.

Build a Culture Worth Staying For

No practice succeeds long term if the people working there do not feel genuinely comfortable and engaged. Comfortable does not mean relaxed to the point of complacency. It means your team shares the practice’s goals, communicates openly with each other, and has the tools they actually need to do their jobs well, from proper equipment to up to date software.

Talking to your staff regularly matters more than most owners realize. Run team meetings, hold one to one sessions, and genuinely ask for feedback rather than treating these conversations as a formality. People want to feel heard, and following through on what they share with real action improves morale, workflow efficiency, and ultimately the experience every patient walks away with.

Frequently Asked Questions

Do I need regulatory registration before opening my private practice?

In most cases, yes. If your practice provides regulated activities as defined under relevant healthcare legislation, registration with the appropriate regulator is required before you can begin treating patients. Confirm whether your specific services fall within scope early, and build the registration timeline into your overall planning.

What kind of medical indemnity insurance do I actually need?

You need coverage that reflects the full scope of your private clinical activity. Any cover held through institutional employment does not extend to private work, so speaking with a specialist indemnity provider before your first private consultation is essential.

How do I get recognized by private medical insurance providers?

Each insurer runs its own recognition process, typically requiring proof of professional registration, indemnity cover, relevant qualifications, and references. Reaching out directly to provider relations teams and allowing several months for processing is standard practice.

Should I hire a dedicated medical secretary or use a virtual assistant service?

Both can work well depending on your consultation volume and budget. A dedicated in house secretary offers consistency and direct oversight, while a virtual or outsourced service is often more cost effective at lower patient volumes. Either way, healthcare administration experience should be a non negotiable requirement.

Final Thoughts

Every private practice will find its own particular path to success, but the fundamentals stay remarkably consistent. Build real systems instead of relying on instinct, protect your legal and financial foundations, invest in the people who support your clinical work, and treat marketing as an ongoing discipline rather than an afterthought. Practices that take these fundamentals seriously tend to build something that lasts well beyond the excitement of opening day.

Running a private practice means wearing two hats at once. One hat belongs to a clinician who trained for years to treat patients well. The other belongs to a business owner who has to handle payroll, compliance, marketing, and a dozen administrative tasks that medical school never covered. Most practitioners are excellent at the first role and completely unprepared for the second, which is exactly why so many clinically brilliant practices still struggle financially.

This guide pulls together the practical side of running a practice: what management actually involves, the early decisions that matter most, the daily habits that separate thriving practices from struggling ones, and the compliance realities that can make or break a business if ignored.

What Practice Management Actually Covers

Practice management is the collection of administrative systems that keep a clinic functioning behind the scenes. It includes hiring and supervising staff, building a referral network, managing budgets, handling billing, and staying current with the tools and standards patients now expect.

This applies whether you run a solo GP clinic, a small multi-specialty practice, a private hospital, or a nursing home. The specific tasks shift depending on the setting, but the underlying principles of organization, financial discipline, and patient experience stay the same across all of them.

Getting the Foundations Right Before You Open

Opening a new practice is a different challenge from managing an existing one. Before you see a single patient, several foundational pieces need to be in place, and getting them right early saves enormous time and cost later.

A written business plan should come first. It needs to define your target patient population, your fee structure, your staffing approach, your premises or remote working setup, and realistic projections for costs and revenue. This document is not just paperwork for a lender. It becomes the reference point for nearly every decision you make in your first year.

Beyond the plan itself, a handful of early steps deserve attention well before opening day. If you are providing regulated healthcare activities in England, registering with the Care Quality Commission is a legal requirement that should be handled early, since the process takes time. If you plan to accept private medical insurance, credentialing with insurers should start alongside your regulatory registration, because paneling can take several months and delays here directly delay your ability to bill.

Your legal and financial structure also needs sorting early: choosing a business entity, opening a dedicated business account, and bringing in an accountant who actually understands medical practices rather than general small business finance. Selecting your practice management software at this stage matters too, since workflows built around the right system from day one are far easier to manage than ones retrofitted months later after habits have already formed. Indemnity insurance suited to your specialty and expected patient volume rounds out the essential early checklist.

Nine Habits That Separate Thriving Practices From Struggling Ones

Treat Your Practice Like a Business, Because It Is One

Providing excellent medical care matters enormously, but it is not the only thing that determines whether a practice survives. Administrative discipline, financial literacy, and operational planning carry just as much weight over the long run.

Building competence in a few core areas pays off repeatedly: solid bookkeeping habits to track every transaction, basic marketing knowledge to keep new patients coming in, human resources skills to attract and retain good staff, and consistent facility management to keep the physical environment safe and compliant. None of this requires a business degree, but investing in even a short course tailored to healthcare providers can close a lot of gaps quickly.

Bring In Outside Expertise Where You Need It

No single person can be an expert in medicine, accounting, employment law, and IT security all at once. Recognizing where your own knowledge runs thin and bringing in a lawyer or accountant for those specific gaps is not a weakness, it is simply good management.

On the operations side, many practice owners eventually weigh whether to bring in a part time operations consultant or a fractional chief operating officer. A consultant typically delivers a one time audit and a set of recommendations, while a fractional COO stays embedded with the practice and helps run the systems on an ongoing basis. Which one fits depends on whether you need a single course correction or continuous operational support.

Protect Your Time Deliberately

Time management determines how much of your day actually goes toward patients versus paperwork. Recent data suggests physicians now spend close to two hours on administrative tasks for every hour of direct patient care, a ratio that has worsened as digital health tools and electronic records have expanded.

Tracking which tasks eat the most time is the first step toward fixing the problem. Automating financial processes that were previously done by hand frees up meaningful hours. Bringing in an administrative virtual assistant to handle scheduling, billing correspondence, and routine email management can also return significant time back to clinical work.

Invest in the People Who Work With You

A practice is only as strong as the team delivering care day to day. Hiring well is the starting point, but retention depends on ongoing support, encouragement, and a genuinely positive working environment.

Implementing basic time and attendance tracking helps prevent burnout by keeping work hours fair and reasonable. Staff who feel undertrained are more likely to make mistakes and experience burnout themselves, which is especially relevant as more daily tasks move onto digital platforms. Regular, ongoing training on whatever software and systems your practice relies on is one of the most direct ways to protect long term quality of care.

Move Away From Paper Records

The vast majority of clinicians in developed healthcare systems have already shifted to electronic health records, and for good reason. Digital records save physical space, cut down on repetitive form filling, and make information far easier to share between providers when a patient is referred elsewhere or seen by a specialist.

Electronic systems also tend to include decision support tools that offer evidence based guidance during diagnosis and treatment planning, something paper charts simply cannot provide. If your practice has not made this transition yet, few upgrades deliver a faster return on the time invested.

Make Care Accessible Beyond the Clinic Walls

Not every patient can physically get to your office. Mobility issues, distance, or periods of illness can all keep someone from attending in person, and without a remote option, those patients often end up seeking care elsewhere.

Telemedicine closes that gap, letting appointments happen regardless of location. Pairing this with an easy online booking system, ideally one a patient can use from their phone, removes friction on both ends of the scheduling process.

Take Data Security Seriously

A security breach in a healthcare setting is not a minor inconvenience. It can permanently damage patient trust, trigger regulatory penalties, and in serious cases lead to litigation that threatens the practice itself.

Basic hygiene goes a long way: regularly updated passwords, secure storage of sensitive information, and staff training on simple but costly mistakes like leaving a workstation unlocked. Many practices now partner with managed IT providers who specialize in healthcare infrastructure, since these providers understand the specific compliance requirements around cybersecurity, cloud storage, and electronic record platforms. Choosing software providers that are explicitly compliant with relevant data protection regulations removes a significant category of risk, and strong information governance is increasingly something regulators expect to see demonstrated, not just claimed.

Get Billing Right the First Time

Medical billing is one of the areas where manual processes cause the most quiet damage. Delayed payments, coding mistakes, and rising claim denial rates all trace back to billing workflows that were never properly systematized.

A dependable billing process verifies insurance eligibility before the appointment happens, captures accurate procedure and diagnosis codes, and submits claims promptly rather than in batches days later. Tracking your claim denial rate matters just as much as submitting claims in the first place, since a structured process for investigating and appealing denials recovers revenue that would otherwise be quietly written off. An integrated system that automates much of this work reduces both the administrative burden and the time it takes to actually get paid.

Make It Easy for New Patients to Find You

Financial health depends on a steady flow of new patients, and for most practices today, that flow starts online. A website optimized for local search results ensures your practice actually shows up when someone nearby searches for the type of care you provide.

Keeping your business listing accurate and current, with correct hours, contact details, and services, matters more than most practices realize. Offering direct online booking removes a common point of friction, letting prospective patients schedule outside normal office hours without needing to call during the day. That small convenience converts far more browsers into booked appointments than a phone-only system ever will.

Understanding Regulatory Compliance and Clinical Governance

Compliance is not optional in private healthcare. It is a structural requirement that shapes nearly every operational decision a practice makes.

In England, most providers offering regulated activities must register with the Care Quality Commission. Meeting CQC expectations means demonstrating that your service is safe, effective, caring, responsive, and well led, the five criteria inspectors use to evaluate any registered provider. Falling short can lead to enforcement action, serious reputational harm, or in extreme cases closure.

Beyond CQC registration, UK practices must handle patient data in line with data protection regulation, covering how information is collected, stored, and shared. Practices with international patients or staff increasingly look to broader information security standards as a useful benchmark alongside domestic requirements.

Clinical governance runs alongside regulatory compliance and covers how a practice maintains and improves care quality over time. This includes structured clinical audits, incident reporting processes, regular staff appraisals, and ongoing professional development. Practices that embed clinical governance into daily operations, rather than treating it as an annual exercise, tend to consistently deliver better outcomes than those simply meeting the minimum bar.

Investing in software with built in audit trails and access controls supports both compliance and governance simultaneously, making it one of the more practical single investments a growing practice can make.

Deciding Between In House Staff and Virtual Support

One of the more consequential decisions in practice management is how to structure your administrative support. The two main paths are hiring in house staff or outsourcing to a virtual medical assistant service.

In house staff offer direct oversight, immediate availability, and a familiar presence that many patients value. The tradeoff is cost. Salary, statutory contributions, holiday and sick pay, and recruitment time all add up quickly, particularly for a smaller practice still building its patient base.

A virtual medical assistant offers a more cost effective alternative for many practices. A capable virtual assistant can handle appointment scheduling, insurance queries, patient correspondence, transcription, and billing without the fixed overhead of a full time hire. Many of these services operate on a percentage of income or a monthly retainer, which keeps costs predictable and scalable as the practice grows.

The right choice usually comes down to patient volume, the complexity of the specialty, and available budget. Many practitioners start with virtual support in the early stages and shift to in house staff once demand justifies the fixed cost. Others land on a hybrid model, pairing one in house coordinator with virtual support for overflow work, which often delivers the best balance of control and flexibility.

What Good Practice Management Software Actually Provides

Whatever structure you choose for staffing, the right practice management software multiplies the effectiveness of the people running your operations. At its core, this type of software handles daily operations including scheduling, online booking, billing, reporting, and inventory tracking.

The features that matter most tend to include a patient portal where people can book appointments, join video consultations, view test results, and message their provider without picking up the phone. Reporting and analytics tools help you see which parts of the practice are performing well and which need attention. Automated payroll reduces the errors that come with manual salary calculations. Inventory tracking keeps consumable supplies accounted for and flags reordering needs automatically. Flexible scheduling tools let you adjust staff calendars quickly from a single place. And a medical customer relationship management layer keeps a full record of patient interactions, supporting both better care continuity and more targeted communication.

Frequently Asked Questions

What does private practice management actually involve?

It covers everything that keeps a clinic running outside of direct clinical care, including scheduling, billing, staff management, regulatory compliance, data security, and financial reporting. In short, it is the business infrastructure that lets a clinician focus on patients rather than paperwork.

Do I need to register with a regulator to open a private practice?

In England, most providers of regulated healthcare activities need to register with the Care Quality Commission before operating legally. Requirements vary by service type, so confirming your specific obligations early in the planning process, ideally with a healthcare regulatory specialist, avoids costly delays later.

Is a virtual medical assistant actually worth the cost?

For practices not yet at the volume needed to justify a full time in house hire, a virtual assistant can provide strong administrative support at a fraction of the cost, covering scheduling, correspondence, insurance queries, and transcription.

What should a private practice business plan include?

A solid plan should cover your service model, target patient population, fee structure, staffing approach, premises or remote arrangements, startup costs, and realistic revenue projections. It should also address compliance obligations directly so governance is built in from the beginning rather than added as an afterthought.

What is the difference between an MSO and general practice management?

A Management Services Organization provides specific administrative or operational support, such as billing, IT, or human resources, while the practice keeps its clinical independence. Practice management, by contrast, refers broadly to the overall administration and business strategy behind running the entire clinic. Many practices use both together, partnering with an MSO for specific backend functions while retaining internal control over overall strategy.

Final Thoughts

Running a successful private practice requires the same discipline as running any other business, layered on top of genuine clinical skill. The practices that thrive long term are rarely the ones with the most advanced equipment or the flashiest marketing. They are the ones with solid financial habits, well trained and supported staff, strong compliance foundations, and administrative systems built deliberately rather than assembled under pressure. Getting these fundamentals right early gives a practice room to grow without constantly firefighting the basics.

API Testing Explained: How It Works and Why It Matters in 2026

Top Software Development Tools to Know in 2026

API Testing Tools: A Complete Guide for 2026

The Transformative Benefits of Artificial Intelligence in Modern Life

AI, SaaS, SEO & Link Building: The New Operating System of Digital Growth

Why Email Marketing Still Drives Real Business Growth in 2026

-

Tech , SaaS3 months ago

Tech , SaaS3 months agoThe Transformative Benefits of Artificial Intelligence in Modern Life

-

Tech , SaaS3 months ago

Tech , SaaS3 months agoAI, SaaS, SEO & Link Building: The New Operating System of Digital Growth

-

Email Marketing3 months ago

Email Marketing3 months agoWhy Email Marketing Still Drives Real Business Growth in 2026

-

Business , Finance3 months ago

Business , Finance3 months agoBusiness & Finance in the Modern World: Strategies, Trends, and Sustainable Growth

-

Sports , Fashion3 months ago

Sports , Fashion3 months agoSports & Fashion: The Perfect Blend of Performance, Style, and Modern Lifestyle

-

Email Marketing3 months ago

Email Marketing3 months agoEmail Marketing in 2026: The Ultimate Strategy for Growth, Engagement, and Conversions

-

Business , Finance3 months ago

Business , Finance3 months agoThe New Economy: How Digital Innovation, Behavioral Finance, and Smart Systems Are Redefining Global Business

-

Health , Education3 months ago

Health , Education3 months agoHealth and Education: The Foundation of a Strong and Successful Society